Takaful Questions Answer: Everything You Need to Know

Takaful Questions Answer: United Insurance Expert mentioned takaful concept in detail.

General Understanding

- What is Takaful, and how does it work?

Takaful is a cooperative system of insurance based on Islamic principles. In a Takaful arrangement, participants contribute to a pool of funds, which is used to support one another in times of need (such as in case of loss, damage, or injury). The contributions are made on a voluntary basis, and the funds are managed in accordance with Islamic law (Shariah). Risk is shared collectively, with the intention of helping participants rather than generating profit for shareholders. - Is Takaful the same as conventional insurance?

While both Takaful and conventional insurance provide financial protection against risks, they differ in structure and principles. Conventional insurance operates on a risk-transfer model, where the insurer assumes the risk in exchange for a premium. In contrast, Takaful operates on a cooperative model, where participants share risk collectively, and profits or surpluses are distributed among them rather than to shareholders. - Why is Takaful considered Shariah-compliant?

Takaful is Shariah-compliant because it is based on principles that adhere to Islamic law. The system avoids elements such as interest (riba), uncertainty (gharar), and gambling (maysir), all of which are prohibited in Islam. Instead, it promotes mutual cooperation, shared responsibility, and ethical investments. - Can non-Muslims participate in Takaful?

Yes, non-Muslims can participate in Takaful. Takaful is based on ethical principles that are not exclusive to Muslims, and anyone, regardless of religion, can benefit from the cooperative structure and the financial protection it offers. - What types of Takaful products are available (e.g., life, health, motor)?

Similar to conventional insurance, Takaful offers a variety of products, including:- Family Takaful (Life Insurance): Provides coverage for life, critical illness, and death.

- Health Takaful: Covers medical expenses, hospitalization, and healthcare-related costs.

- General Takaful (Motor, Property, etc.): Covers risks such as damage to property, motor vehicles, and more.

Financial & Operational Aspects

- How are Takaful contributions (premiums) used?

In Takaful, contributions (known as “tabarru”) are pooled together to form a fund that is used to provide financial protection to participants in case of a claim. The fund is managed in a manner that ensures it adheres to Islamic principles, with investments being made in Shariah-compliant assets. One portion of the contribution is given to the company as the management system (Wakala Fee), and the rest of the amount goes to participant funds. - What happens if I don’t make a claim—do I get any money back?

If a participant does not make a claim, they may be entitled to a portion of the surplus or profits generated by the Takaful fund, depending on the terms of the policy. In some cases, the surplus may be returned to participants or used to reduce future contributions. - How is profit or surplus distributed among participants?

The surplus or profit generated by the Takaful fund is distributed according to a pre-agreed formula. This distribution can vary, but typically it is shared among the participants based on their contributions. Some models may allow for a percentage of the surplus to be distributed to participants as a rebate, while others may reinvest it to reduce future contributions. - Does Takaful cover the same risks as conventional insurance?

Yes, Takaful covers many of the same risks as conventional insurance, including health, life, motor, and property risks. The difference lies in how the risk is managed and how profits are distributed. In Takaful, the focus is on mutual cooperation, and funds are not used for investment in unethical industries. - How does Takaful ensure transparency and fairness?

Takaful ensures transparency and fairness by following principles of accountability and open communication. Shariah-compliant governance structures, regular auditing, and the involvement of Shariah supervisory boards help ensure that the funds are managed ethically and in line with Islamic principles. Additionally, the distribution of surpluses and profits is clearly defined and agreed upon in advance.

Technology and Takaful

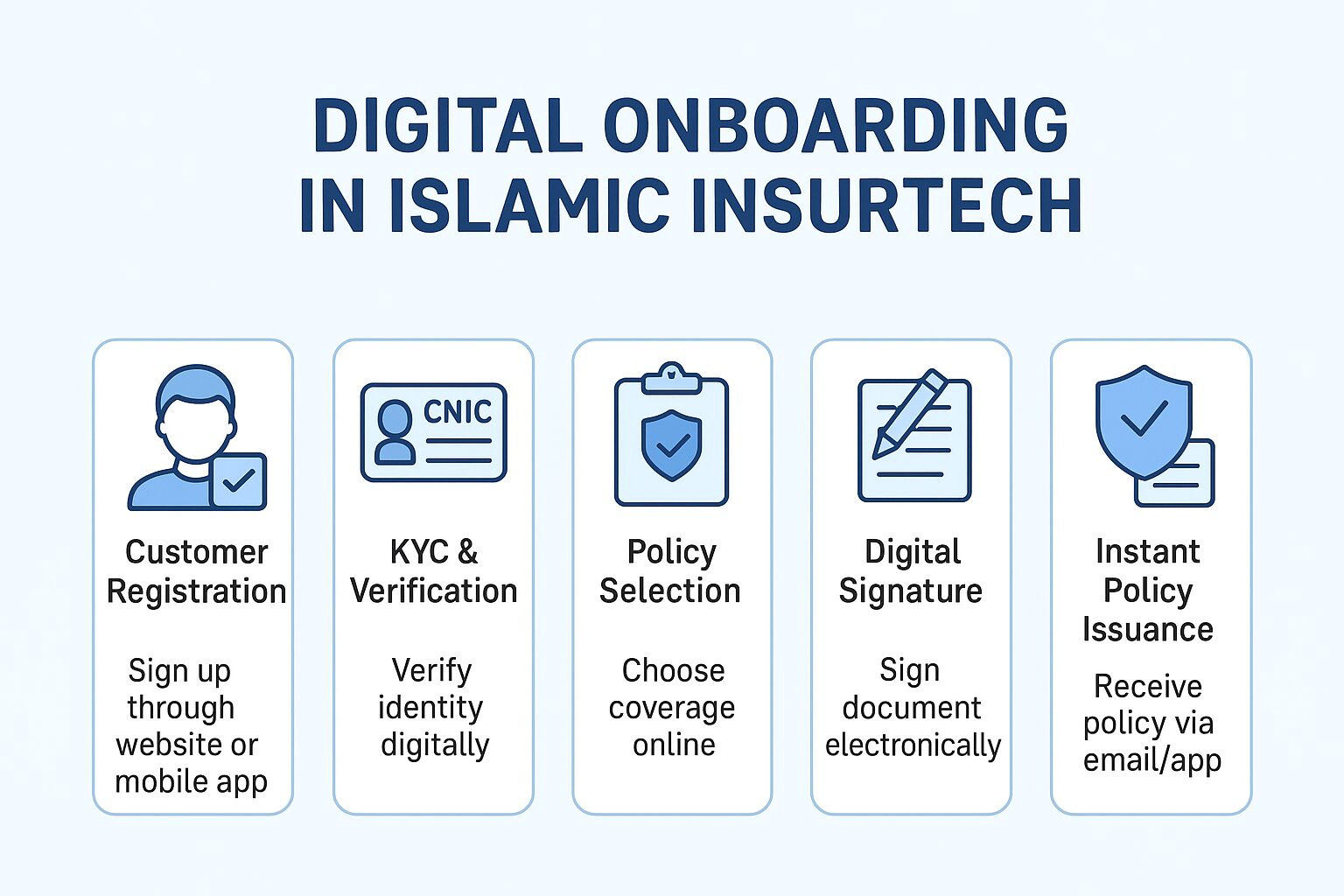

- How is technology improving Takaful services?

Technology is significantly enhancing Takaful services by improving efficiency, transparency, and accessibility. Digital platforms enable easier customer onboarding, policy management, and claims processing. AI-powered tools help assess risks more accurately, while automation speeds up administrative tasks. Moreover, advanced data analytics can help providers personalize policies to better meet participants’ needs and improve customer experience. - Can I buy and manage Takaful policies online?

Yes, many Takaful providers now offer online platforms or mobile apps where customers can purchase policies, make contributions, and manage their Takaful plans. These platforms allow for seamless interaction, making it more convenient for participants to track and update their policies, file claims, and get customer support—all from their devices.

Takaful Questions Answer: United Insurance Expert

Watch insightful videos of the above Takaful expert in Takaful Questions Answer on our YouTube channel.