InsurTech in the takaful & insurance sector of Asia and Pakistan:

Pakistan’s growing population and middle class benefit its insurance markets. Pakistan has Asia’s third-lowest insurance subscriptions (Peak Re, 2020). The Insurance Association of Pakistan reports a 0.03% premium to GDP. Takaful contributes 0.006% to GDP and a premium of 0.22 percent. Pakistan has five public sector insurance companies, fifty private, and five foreign companies. Twenty-nine of sixty offer non-life insurance, and seven offer life insurance (Economic Pakistan, 2008).

Insurance contracts provide financial security or refunds for damages (Jamapunji, 2018). Thus, a conventional insurance company sells a policy against premium to the insured for a specific risk in a specified period with a defined compensation limit (Spaulding, 2020). Pakistan’s conventional insurance industry struggles with awareness, risk assessment, operational inefficiencies, and old tariff structures (Global Village, 2020; Cortis et al., 2018). Marine insurance began in Italy in the 13th century (Spaulding, 2020).

Edward Lloyd’s 17th-century London coffeehouses pioneered underwriting. Traders, merchant ships, and others seeking coverage gathered there. Edward Lloyd gave clients dockyard shipment data. In 1769, the official underwriters accepted marine risks here (Greene, 2019). Takaful (Insurance) differs from conventional insurance because Shariah prohibits Gharar (uncertainty), Maisir (Gambling), and Riba (Interest) (Billah, 2019).

Pakistan, founded on Islam, introduced Islamic finance to eliminate Riba. Pakistan took action in the 1980s. It failed due to a lack of workforce skills and training. Pakistan introduced Islamic finance in 2000. Pakistan has 22 Islamic banks—six full-fledged and 17 conventional with Islamic banking divisions. Pakistan has five Takaful companies and 80 Islamic mutual funds (Hanif & Iqbal, 2017). Five Pakistani takaful operators offer Islamic insurance (Alhuda, 2020). Islam governs Takaful. Ta’awun (mutual support) and tabarru’ (voluntary contribution) share risk. Pak Qatar, Pak Kuwait, and Takaful Pakistan offer general takaful, while Pak Qatar Family Takaful and Dawood Family Takaful offer family takaful (Jamapunji, 2020).

Takaful comes from aqila (tribal fund) and diyah systems (blood money), where a tribe rescued a member who had to pay blood money (diyah) (Manjoo, 2019). If a different community member killed someone, their relatives paid blood money to the tribe whose man was killed. Prophet PBUH approved the aqila system (tribal fund). This mutual aid system established takaful (Zainuddin & Noh, 2013). Family and General Takaful exist (Billah, 2019).

Takaful operations first started in Sudan by using the Wakalah – Mudarabah model, whereby Wakalah (delegation) is used for underwriting activities, and Mudarabah (partnership) is used for investment activities (Al-Dhareer, 2004). General takaful took place first in Sudan in 1979. Then it was fashioned for the Middle East markets by the early 1980s, including the UAE in 1980, Saudi Arabia in 1983, Bahrain in 1989, and Qatar in 1995. Two leading models are Mudarabah, which is extensively used in Asia, and Wakalah, which is widespread in the Middle East (Smith, 2007).

Pakistan’s takaful companies use Wakalah-Waqf. Pakistani takaful companies are financially weaker than conventional insurers (Hanif & Iqbal, 2017). Pakistan’s takaful industry faces a lack of innovative products, awareness (Hanif & Iqbal, 2017), adoption of innovative and customer-friendly technology, customer access, especially in rural areas (Jubilee, 2015), and regulatory statute ambiguity (Dawood Takaful, 2019). Pakistan’s conventional insurance faces risk miss-assessment, operational inefficiencies, and an old tariff structure (Torben et al., 2018).

Islamic scholars believe digital technologies can help Islamic insurance/takaful develop society. Blockchain and crowdfunding can help Islamic banks and insurers market financial services, increase financial inclusion, and improve service (IRTI, 2019).

Due to a more educated, working-age population and growing awareness of takaful and its religious orthodoxy, takaful insurers in ASEAN and the Middle East have more opportunities to use digital innovation to improve operational efficiency and target more Islamic countries. As Saudi Arabia and UAE develop communication and information technology infrastructure, especially in high connectivity, the Middle East will have 160 million digital users by 2025. (The European, 2017).

Conventional and Takaful insurance has high costs, from labor to the final price. Technological disruption will make insurers’ business models unsuitable in 20 years (Daniele, 2019). Science and technology have no religion, so InsurTech can solve all takaful and insurance problems (Khalid, 2001).

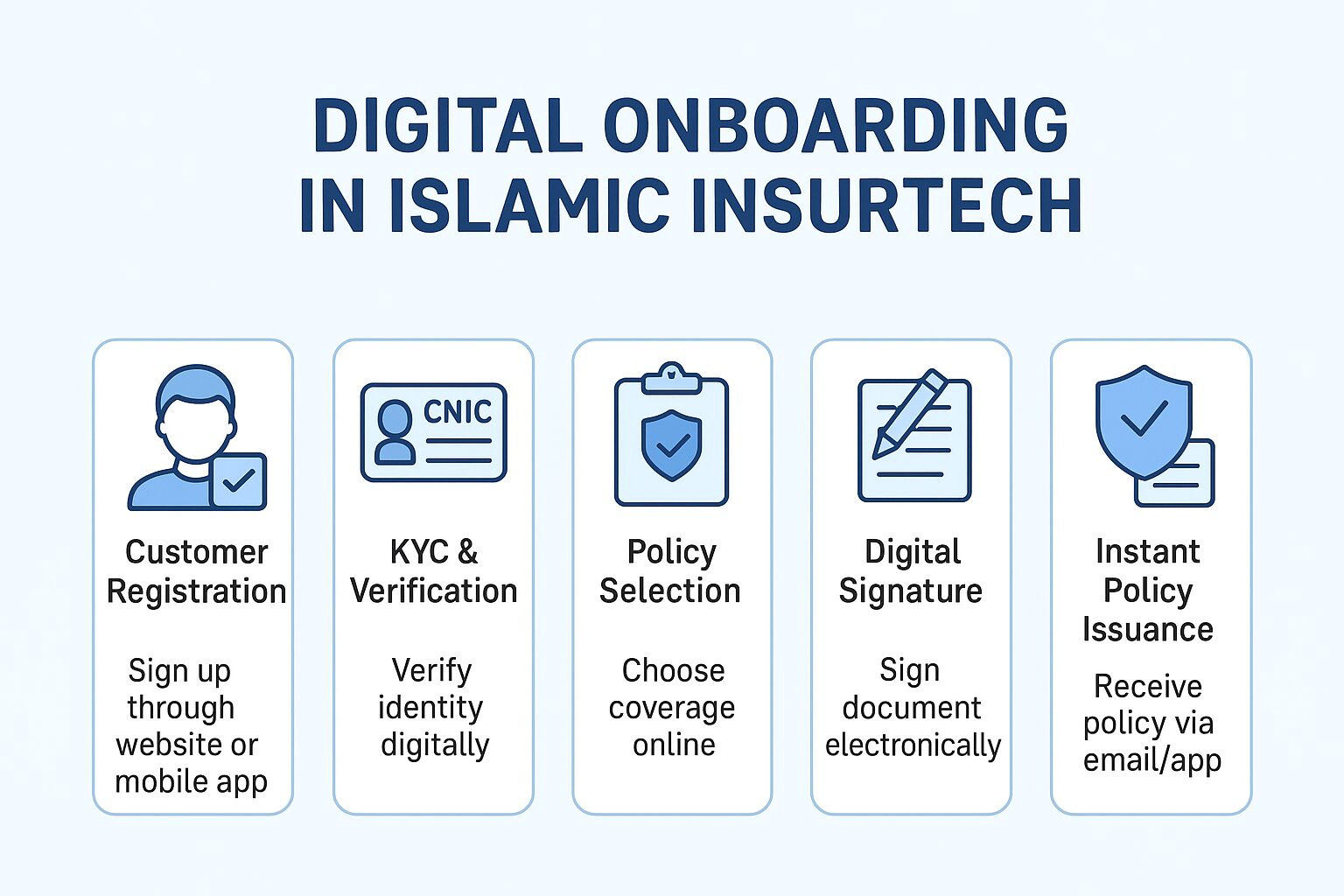

InsurTech can address insurance industry issues to boost penetration. Customer relationship management, pricing compilation, multi-channel distribution, digital claim processing, and online insurance purchasing are simplified. Auto telematics, environmental sensors, and home security are new ways insurers can earn. Wearable health insurance services have changed. Insurers can now reduce risk and offer a new product with flexible screening and customized premiums. Digital saving plans and pension management help insurers manage wealth. Smart digital agreements, KYC, and automated processes reduce compliance costs (Yan et al., 2018).

The enormous populace, growing internet and smartphone diffusion, and a relaxed regulatory environment make a good case for InsurTech in Pakistan. Insurance, especially micro-insurance penetration, can be grown by using insurance technology, as this market is still lagging in Pakistan because of the challenge of its availability for conventional financial service providers (Recorder, 2018).

InsurTech is a set of novel financial technologies. It permits insurers to expand their product ranges and create alternative sales channels targeting existing and potential clients. For example, micro-insurance Targetsoor health and crop insurance marketing mobile phone technology (Myanmar Financial Services, 2019). Despite the benefits of adopting InsurTech, there is a need to explore the challenges regarding adopting this technology in Pakistan’s takaful and insurance sectors.

Pakistan’s IT adoption faces the following issues: inconsistent IT policy, negative and uncooperative administrative machinery, weak implementation, bureaucratic IT ignorance, legal infrastructure issues, and a lack of qualified IT professionals (Kundi et al., 2008). This study examines InsurTech adoption challenges in the Pakistani insurance industry (takaful and conventional), which must be addressed. Otherwise, foreign FinTech companies (MicroEnsure, BIMA) and Pakistani FinTech companies (Karlocompare, Smart Choice, and Mawazna) could capture the insurance market by providing insurance from forward to backwards in the insurance value chain business model.

Without InsurTech, the insurance business would struggle to survive. In the next five years, PwC Global FinTech predicts that 25% or more insurance companies will lose market share due to FinTech competition (PwC, 2020). InsurTech, a FinTech branch, can solve insurance industry problems. PWC found that 74% of insurers feared FinTech disruption. 68% of insurers used FinTech to collaborate to solve problems (PwC, 2016b).

This study addresses InsurTech adoption in Pakistan’s insurance industry (takaful & conventional insurance). Targeting unserved and existing market segments with innovative technologies helps increase insurance penetration, which is currently less than 1%.