Pakistan’s Insurance Penetration:

Pakistan’s insurance penetration is less than 1%, compared to the US’s 30% and India’s and Bangladesh’s 5-6 percent (Global Village, 2020). There is low penetration in insurance/takaful industry which can be enhanced by adopting advance technologies.

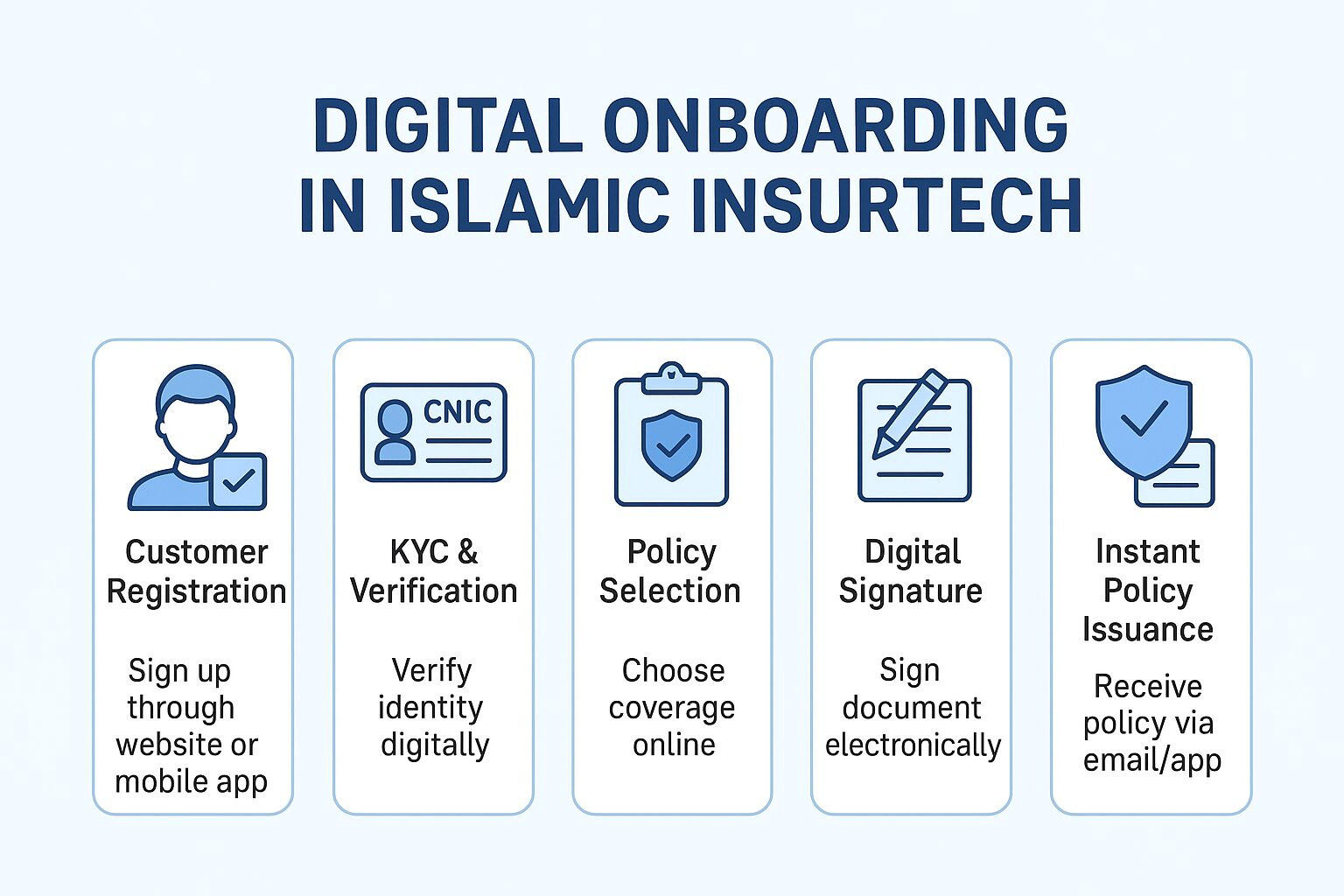

These advance technologies if applied in insurance sector then called InsurTech. InsurTech/FinTech adoption has also a lot of challenges which are explored in the context of Pakistan in terms of literature, secondary videos of InsurTech experts and insurance/InsurTech experts working at management level in takaful and insurance sector of Pakistan.

Pakistan’s rural, poor and women face financial exclusion. Financing rural communities is complex due to high costs and traditional banking infrastructure. Low-cost digital financial services from FinTech can solve this.

InsurTech and TakafulTech:

Digital channels allow InsurTech/fintech and TakafulTech to offer affordable insurance to Pakistan’s uninsured. Pakistan launched its first National Financial Inclusion Strategy in 2015 to reach 50% of adults by 2020. FinTech can serve Pakistan’s rural, youth, and women markets. Digital financial inclusion could boost Pakistan’s GDP by $36 billion by 2025 (Mohsin & Hussam, 2021). Asia is leading the technological revolution. The global middle class will grow 180 percent between 2010 and 2040 (PricewaterhouseCoopers, 2020).

Financial Services in InsurTech and TakafulTech:

Financial services include indemnification, money management, disbursements, and digital banking. Financial institutions offer personal, consumer, and corporate services. Transparency and fairness are maintained by independent agencies (Phaneuf, 2020). Technology affects financial services processing. Banks use modern technology to provide excellent customer service (Frometa, 2019).

The latest trends of technology in financial services are the following (PwC, 2020):

- FinTech (financial technology) or InsurTech (insurance technology) drive the new business model.

- Blockchain shakes things up due to its vital role in the operational infrastructure of financial institutions.

- Customer intelligence uses analytics on collected customer data to identify the actual need

- Robotics and AI replace bank tellers.

- The public cloud is known for its infrastructure model for non-core business processes, i.e. Customer Relationship Management (CRM), human resources, and fiscal book-keeping.

- Cyber-security is famous in the current era for abating financial relating perils.

Latest Trends of Technology in Insurance Sector:

Blockchain, Big Data, and Smart contracts in the insurance sector are revolutionizing assurance services (Yu & Yen, 2018). The lack of high-tech assurance applications raises operational costs, creating a need for new technology. Computerization can reduce document storage, recovery, and processing costs without human intervention (Tapscott & Tapscott, 2016). Chat apps and video conferencing simplify customer engagement (Khristy, 2019). Online services and products are being innovated by technology. It also improves data collection to identify and mitigate risks, payment, and claims management (OECD, 2017). InsurTech applications improve insurance management and customer engagement (Tapscott & Tapscott, 2016). InsurTech has improved insurance companies’ internal operations, controls, supervision, policy, and decision-making (Simon, 2019). FinTech has affected banks, insurance, e-payments, and money management.

FinTech Evolution:

60% of lending institutions and 49% of banks in America consider FinTech corporations essential. 25% of FinTech is in digital payment (Tipalti, 2020). Figure 1 shows FinTech’s evolution. FinTech 1.0 began in 1886-1967 when telegraph and railways transferred financial information. Online banking began in 1967-2008 with bank mainframe computers and networks. Smartphones, 5G Technology, Bitcoin, Blockchain, Google Pay, Apple Pay, and other technologies are used in FinTech 3.0, which began in 2008. China uses FinTech 69% and India 52%, so FinTech 3.5 is for emerging markets (Ziggurat, 2020).

FinTech in Pakistan:

Pakistan is in FinTech 3.5 due to the lack of traditional and emerging FinTech. Most of FinTech is in banking and insurance. Due to its young population, internet access, and rising mobile subscriptions and digital trading, Pakistan’s FinTech market has great potential (Kumail et al., 2008). Lahore, Karachi, and Islamabad have a few FinTech companies. Pakistan’s FinTech ecosystem faces data security, IP, and regulatory uncertainty (Shahid et al., 2016).

Figure 1 – FinTech evolution. Source (Ziggurat, 2020)

Pakistan has the sixth-highest population and a cash-based economy. Pakistani FinTech has revolutionized payment system technology, increasing financial inclusion. FinTech collaborates with banks, which have more customers. For instance, FINCA Microfinance Bank and Finja FinTech startup started a branchless mobile wallet app (Kumail et al., 2008). The State Bank of Pakistan (SBP) reported 287 million mobile and internet transactions in FY 2020–21, totaling PKR 10.5 trillion. Over the previous year, transaction volume and value increased by 106 percent and 124 percent, respectively.

E-commerce transactions quadrupled during this time. Pakistan is rapidly adopting digital payments. The State Bank’s Raast payment system may accelerate this trend. Raast is overhauling its back end, and instantaneous interbank money transfers will benefit customers. 1-Link Network processing delayed about 3% of transactions for several days, causing unnecessary stress for senders and receivers. Most importantly, Raast lets you make money-collecting aliases. Like EasyPaisa and JazzCash, a mobile phone number is needed to send and receive money. Raast’s accessibility and reliability will encourage digital payments. Raast requires your bank’s mobile app, which is the problem (Asad, 2022).

Overall, this article explores the challenges behind the low adoption level of InsurTech/FinTech in the insurance sector and takaful sector of Pakistan, where insurance penetration is less than 1%. Studies in other countries pointed out that it is due to less awareness, manual working, outdated technology, lack of resources, long claims processing, bogus claims and other fraud cases. This study posits that InsurTech can significantly increase insurance penetration by more than 1% in Pakistan via cost effectiveness, innovation and customer satisfaction. There are few InsurTech startups which are working in Pakistan, and the IT adoption rate is also less. There are also companies like statefarm insurance, a US based company which adopted IT to smooth its operational works.