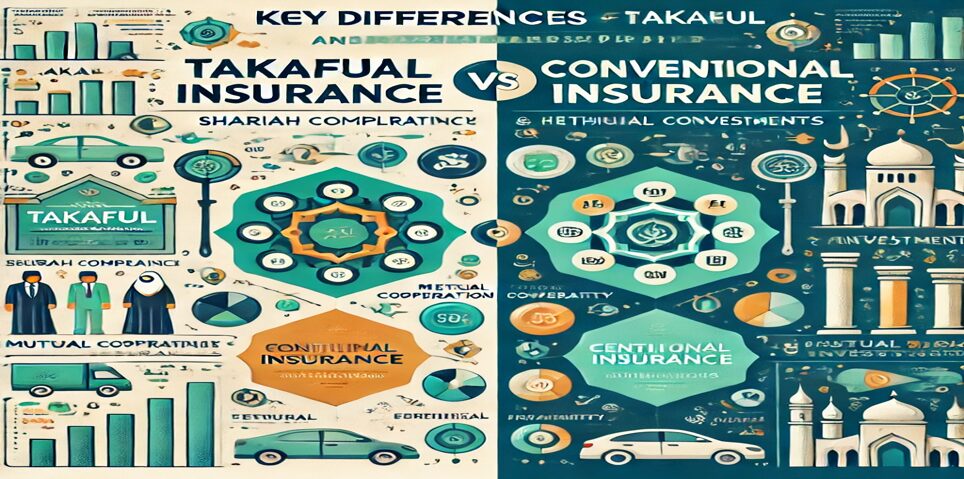

Key Differences Between Takaful and Conventional Insurance by 5th Pillar Expert described in following points. Takaful is a Shariah-compliant insurance model based on mutual cooperation, where participants contribute to a shared pool to support each other in times of need. This system contrasts with conventional insurance, which involves an insurer assuming financial risk in exchange for premiums.

What are the Key Differences Between Takaful and Conventional Insurance by 5th Pillar Expert?

-

Ethical Foundations in Takaful vs Conventional Insurance:

Takaful operates in full compliance with Islamic principles by avoiding riba (interest), maysir (gambling), and gharar (uncertainty). Conventional insurance, on the other hand, may involve these elements, which are prohibited in Islam. -

Risk Sharing Model: In Takaful, the risk is shared among participants, where everyone contributes to a pool that covers claims. This collaborative model promotes mutual assistance, unlike conventional insurance, where the insurer assumes the financial risk. This model makes Takaful more ethical and inclusive, as all participants benefit together.

-

Shariah-Compliant Investments: Funds in Takaful are invested in Shariah-compliant assets like sukuk, real estate, and equities. Unlike conventional insurance, which may invest in non-Islamic ventures, such as alcohol, gambling, or tobacco, Takaful follows Islamic finance guidelines to ensure its investments align with ethical principles.

-

Contributions and Surplus Distribution: Contributions from participants fund the shared pool for claims, operational costs, and Shariah-compliant investments. Any surplus after claims and expenses may be distributed among participants or reinvested based on predefined ratios. Conventional insurance typically retains surplus profits for the company.

-

Transparency and Ethical Practices: Takaful emphasizes transparency in pricing and operations, with all fees clearly outlined. Unlike conventional insurance, where terms may be unclear or involve hidden charges, Takaful ensures that all costs are easily understood by participants.

-

Shariah Board Oversight: A Shariah board oversees the Takaful process to ensure operations comply with Islamic law. This oversight is absent in conventional insurance companies, where ethical practices are not always guaranteed.

-

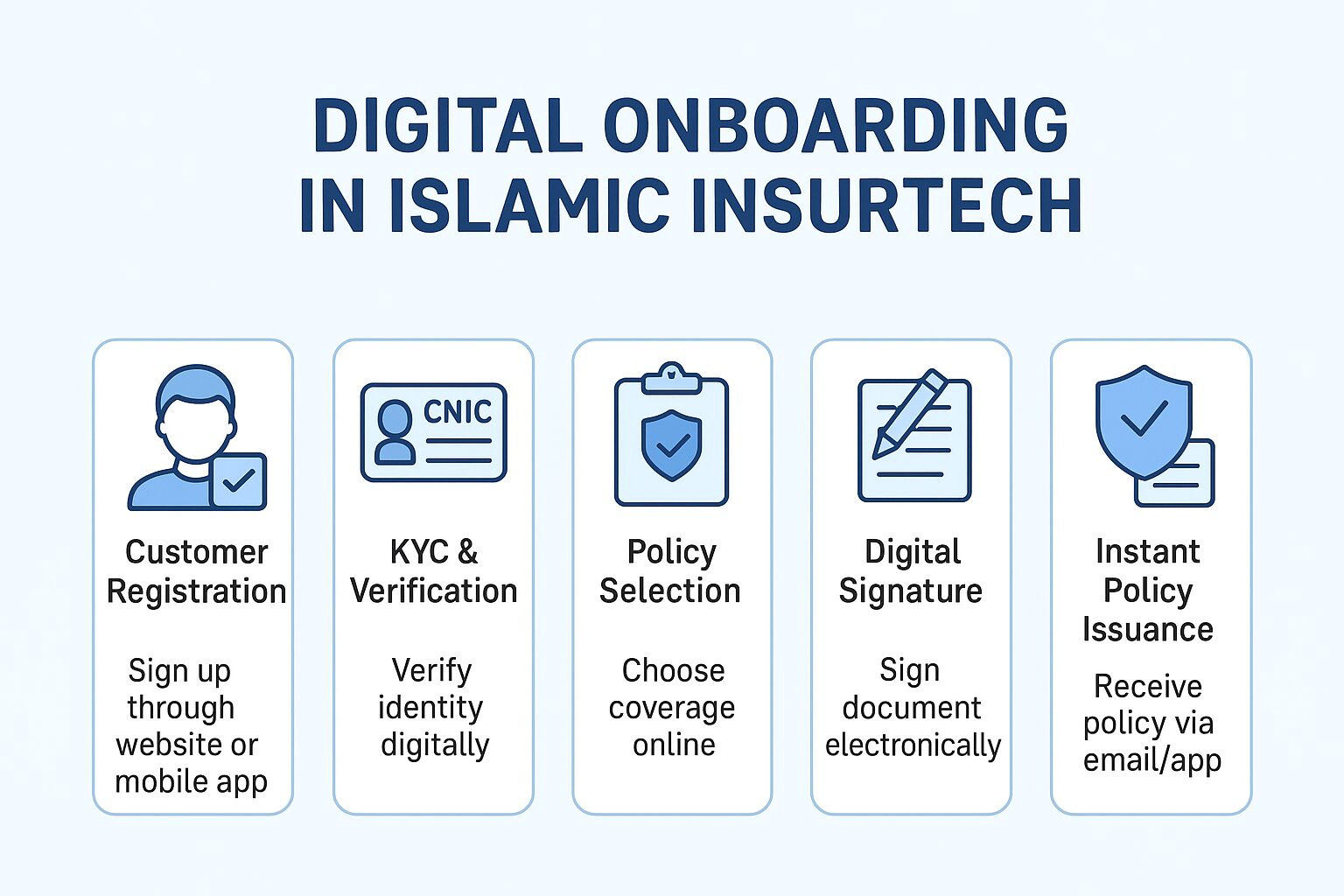

Technology in Takaful vs Conventional Insurance: Technology plays a significant role in the accessibility and efficiency of both Takaful and conventional insurance. Many Takaful providers offer digital platforms for policy management and claims. AI, blockchain technology, and mobile apps streamline processes in both models, but Takaful ensures that these technologies uphold ethical standards.

-

Open to All: Takaful is open to everyone, regardless of religion. While it adheres to Shariah principles, it focuses on mutual cooperation and ethical conduct, making it available to people of all faiths. Conventional insurance, while open to all, may not follow ethical principles in its operations.

-

Financial Security and Bankruptcy: In the rare event of bankruptcy, Takaful funds are protected through reserves and reinsurance, ensuring that participants’ contributions are safeguarded. Conventional insurance companies may not offer the same level of financial security.

-

Awareness and Popularity of Takaful: Limited awareness and fewer providers contribute to Takaful’s lower popularity in some regions. However, as more people recognize its ethical and Shariah-compliant benefits, Takaful is gaining more traction worldwide.

Key Differences Between Takaful and Conventional Insurance by 5th Pillar Expert

Conclusion: Key Differences Between Takaful and Conventional Insurance by 5th Pillar Expert

Understanding the key differences between Takaful and conventional insurance by 5th Pillar Expert is essential for individuals looking for an insurance model that aligns with Shariah principles. Takaful offers an ethical alternative to conventional insurance, focusing on mutual assistance, transparency, and compliance with Islamic law.