InsurTech History:

InsurTech stands for insurance technology. The insurance sector is now adopting advanced technologies like cloud computing, big data analytics, blockchain, artificial intelligence, IoT, mobile, drones, machine learning, deep learning, and many more. There are also InsurTech startups that are facilitating the insurance sector in adopting the above-mentioned technologies. This article discusses the history of insurance from the perspective of the Industrial Revolution which ended with Industrial Revolution 4.0 in which the smart city concept, e-services, and robotics were introduced to the world.

First Industrial Revolution (Insurance 1.0):

Insurance predates Christ (BC). Risk transfer and distribution were used by 3rd- and 2nd-millennium BC traders. Chinese merchants split their goods among many boats to reduce the risk of a shipwreck. About 1750 BC, Mediterranean maritime traders adopted the Babylonian Code of Hammurabi method. A merchant pays a fee to the lender to cancel the loan if the cargo is stolen or lost at sea. Rhodesians invented the “generic average” around 800 BC. Companies may ship together. Merchants who lost goods in a storm or shipwreck received premiums (Trenerry, 2009).

Modern house insurance began with the 1666 Great Fire of London, which destroyed over 13,000 homes. Industry means organized, systematic work. Roman brickmaking is a great example. Western Europe, North America, and the world, were transformed by James Watt’s 1782 steam engine. Maritime, rail, and air transport increased. The Railway Passengers Assurance Company was founded in England in 1848 to cover rising railway deaths (McNabb, 2016).

Second Industrial Revolution (Insurance 2.0):

Technology like electricity and the telegraph helped enhance transportation and communication. Steel, copper, and aluminum were required for machine manufacturing, broadening the industrial idea, notably in chemistry (Schwab, 2017). Governments started national insurance programs in the 19th century to safeguard workers from sickness and old age. Germany leaned on 1840s Prussian and Saxony social programs. In the 1880s, Chancellor Otto von Bismarck introduced old-age pensions, accident insurance, and medical care (Hennock, 1997).

Third Industrial Revolution (Insurance 3.0):

Introducing computer-based applications to help the company. Early computer uses were in actuarial and statistical sciences. Other insurance process management applications were also launched. Until increased productivity and reduced costs, most independent agents used desktop computers from the early 1980s to the mid-1990s. Since 1970, Acord, an American non-profit standards-setting body for the insurance industry, has included automation. Companies, agents, suppliers, solution providers, organizations, and others are members. They provide both conventional and EDI formats (Shaw & Qualls, 2005).

Fourth Industrial Revolution (Insurance 4.0):

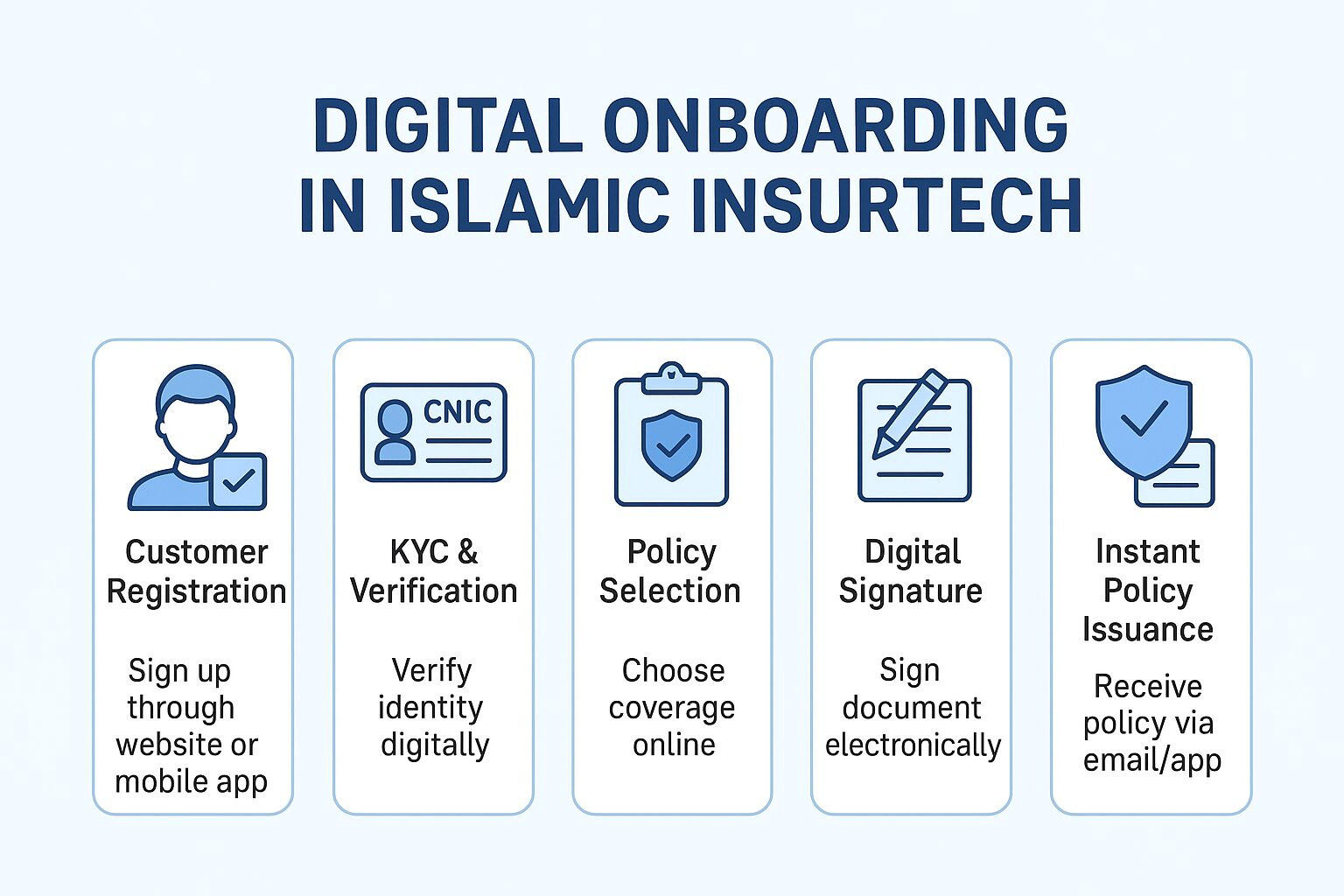

The Internet revolutionized society. IoT, improved software, and equipment automation ushered in the fourth industrial revolution (Kagermann et al., 2013). Examples include on-demand, usage-based, peer-to-peer, cyber, and business interruption insurance. Any major messaging platform can use an AI chatbot. People use WhatsApp, Facebook Messenger, and Instagram daily. Customers can buy insurance online, via email, live chat, mobile app, text, forums, and social media. Billboards, TV, and newspaper ads promoted insurance contracts in the past. 38 Sponsorship, articles, and social media are innovative insurance advertising methods (such as Facebook and LinkedIn). Paperless processing eliminates commissions and administrative costs on this direct route.

Price comparison websites (PCW) aggregate plans from multiple insurers and display them by price to help people find insurance quickly. Big data analytics in insurance enhances customer service and financial aid. Drone photos speed up, simplify, and improve claims processing. Cloud computing removes data center constraints. The pandemic may drive more cloud systems and applications (Bernardo, 2021).

Overall, the Industrial Revolution brought changes in many industries including insurance which not only changed the business model but also opened many avenues in terms of product innovation, customer engagement, customer satisfaction, operational efficiency, fast claim administration, reimbursement and underwriting, and much more.